The Hispanic Housing Bubble in Graphs

Steve Sailer, VDARE, February 15, 2015

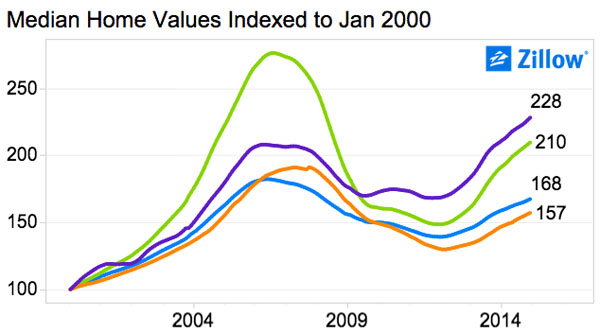

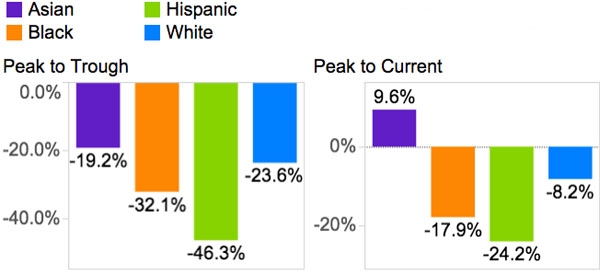

I may have pointed out once or twice that the disastrous home price bubble of a decade ago was closely intertwined, via numerous causal pathways, with decades of Hispanic immigration and diversity ideology. Here’s a new graph from a report by Zillow on different ethnic neighborhoods that makes my point for me: The green line represents the median home value in Hispanic neighborhoods and the blue line white neighborhoods across the country. The green line soared out of control before dropping 46.3% (and still being down 24.2%).

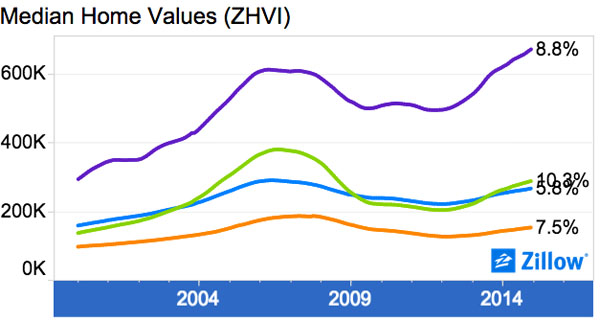

It’s widely assumed that the Hispanic Tidal Wave we are always hearing about regarding elections couldn’t possibly have had any impact on home prices because Hispanics are so few in number and so poor, but during the bubble, the median home prices in Hispanic neighborhoods was higher than in white neighborhoods, nationally. Here’s median home values in thousands of dollars:

You can see the on-going Chinese Money Laundering boom in the purple (Asian) line.

You can look up your own metropolis on Zillow’s handy page.

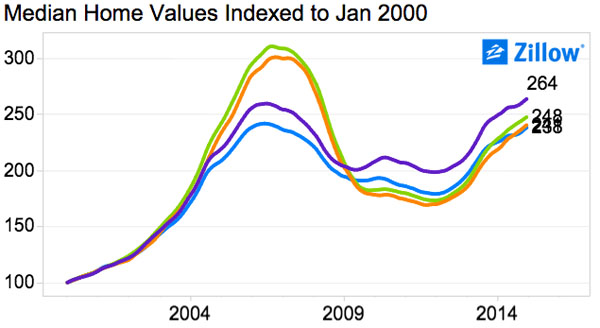

Here’s the enormous Los Angeles metropolitan area indexed to 2000=100. Versus their peak, white neighborhoods in Greater L.A are currently down 1.6% in median home price, while Hispanic and black neighborhoods are still down over 20%:

For example, from the Boston Globe, here’s a report on Boston:

Hispanic areas lag in housing recovery

By Katie Johnston GLOBE STAFF FEBRUARY 09, 2015

Hispanic communities were particularly vulnerable to unscrupulous lenders during the last housing boom and the hardest hit by the bust, experiencing the sharpest drop and slowest recovery in home values, according to a study to be released Monday.

The study, by the online real estate company Zillow, found that . . . Nationwide, Hispanic areas also suffered the biggest declines, with home values still down 24 percent from their peak nearly a decade ago, according to the study.

Hispanic neighborhoods tend to have higher populations of immigrants who were first-time home buyers and were put at risk by lenders who waived credit checks and minimum-income levels, housing specialists said.

Many of these subprime loans were for multifamily homes, which are popular among low-income residents because they can rent out units to generate income.

All of this activity led to an increase in home sales and skyrocketing prices in lower-income neighborhoods. But then the housing bubble burst in the middle of the last decade, the financial crisis followed, and many workers lost jobs.

The result: People who were barely making mortgage payments before the recession went into foreclosure, causing home prices around them to plummet. . . .

“It’s the old story of what goes up fastest falls fastest,” said Barry Bluestone, director of the Dukakis Center for Urban and Regional Policy at Northeastern University.

Yanko Matias, a native of the Dominican Republic, wanted a house where he and his wife could raise their two young children. So they bought a single-family home in Lynn in 2007, taking out a loan for the entire purchase price of $232,000.

But in early 2009, Matias lost his landscaping job. He found another job at a rental company, but was making considerably less money and called the bank about modifying his loan to reduce the payments. The bank refused, telling him his house was worth only $180,000, less than what he owed on his mortgage.

By the end of the year, he was in foreclosure.

Matias, 39, who now works as a taxi driver and still lives in the house, has been fighting the bank ever since. But he has little hope his home will regain its value and fears he will eventually lose it.

“I worry every day about it,” he said.

To analyze housing values, Zillow used Census data to categorize ZIP codes by racial or ethnic groups that make up a plurality of the population and estimated the median home value within each area. . . .

Many housing specialists, however, see the uneven housing recovery breaking down not by race, but by immigrant status.

“They were basically the most innocent consumers on the marketplace,” said Eloise Lawrence, a staff attorney at Harvard Legal Aid Bureau who works with struggling Lynn tenants and homeowners. “They knew the least about what was happening, and they were the most eager to climb onto the first rung of the American dream.” . . .

As disconcerting as it is that Hispanic homeowners were hurt so much by sagging home values, Lawrence, of the Harvard Legal Aid Bureau, said the recovery of home values in white and black communities is almost as worrisome: “We may be in another speculative bubble.”